| Analysis of Times Series with Stata |

| 2. Computing seasonal components and predicting with an additive series |

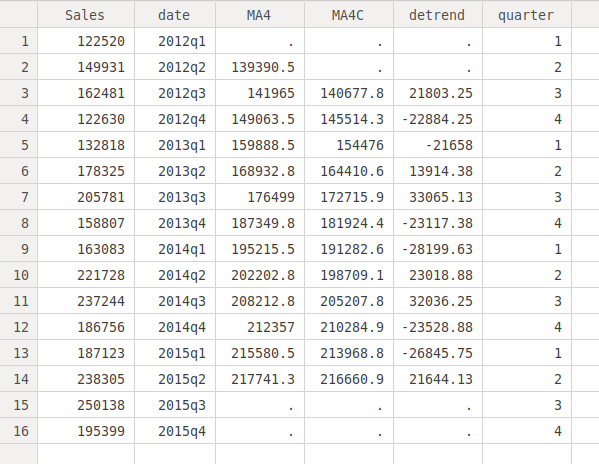

generate detrend = Sales - MA4CTo eliminate the irregular component, we have to take a mean of the "detrend" variable we have just created within each quarter. To do this, we first generate a variable called "quarter" indicating the quarter:

gen quarter = quarter(dofq(date))Let's see the variable we have created:

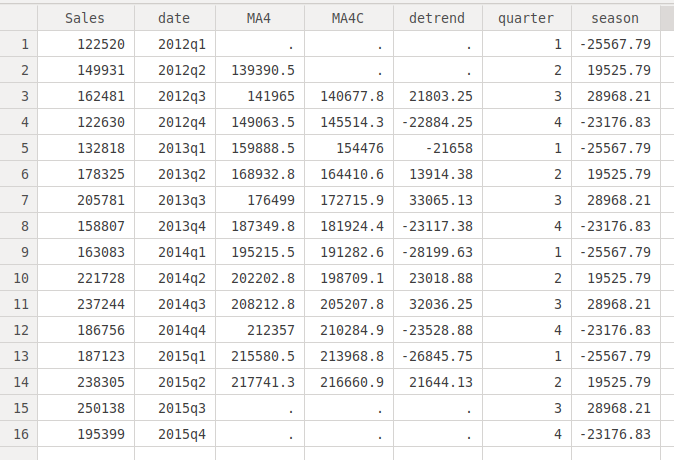

bysort quarter: egen season = mean(detrend) sort dateThe first command computes the means by quarters, and the second one reorders the cases according to time since the first command disorders them. If we know look at the quarters, we can see that we have same seasonal component for each quarter:

. reg Sales date Source | SS df MS Number of obs = 16 -------------+------------------------------ F( 1, 14) = 21.34 Model | 1.5120e+10 1 1.5120e+10 Prob > F = 0.0004 Residual | 9.9174e+09 14 708386771 R-squared = 0.6039 -------------+------------------------------ Adj R-squared = 0.5756 Total | 2.5037e+10 15 1.6692e+09 Root MSE = 26616 ------------------------------------------------------------------------------ Sales | Coef. Std. Err. t P>|t| [95% Conf. Interval] -------------+---------------------------------------------------------------- date | 6668.61 1443.43 4.62 0.000 3572.761 9764.46 _cons | -1255019 311130.3 -4.03 0.001 -1922327 -587710.5 ----------------------------------------------------------------------------At the last two lines we can see the values for the constant and the slope of the linear trend. To obtain a prediction adjusted for seasonality, we have to first figure out the value of "date" for the quarter we want to predict. Stata codifies dates ("date" is our variable) with an internal number. To see the number corresponding to the third quarter of 2016, we enter:

di tq(2016q3)Stata tells us that this number is 226. We now predict the trend for the third quarter of 2016:

. adjust date = 226 ----------------------------------------------------------------------------------- Dependent variable: Sales Command: regress Covariate set to value: date = 226 ----------------------------------------------------------------------------------- ---------------------- All | xb ----------+----------- | 252087 ---------------------- Key: xb = Linear PredictionTo adjust the seasonal component we first figure out its value for the third quarter, asking Stata to show us the value of "season" but only for the third quarter:

. list season if quarter == 3 +----------+ | season | |----------| 3. | 28968.21 | 7. | 28968.21 | 11. | 28968.21 | 15. | 28968.21 | +----------+And finally we obtain the prediction adjusted by the sesonality:

. di 252087 + 28968.21 281055.21Sales of ice cream are predicted to be 281055.21 for the third quarter of 2016.